Velocity Banking

Velocity banking is a proven debt elimination strategy that helps you pay off your mortgage or other loans early—often years faster than traditional methods.

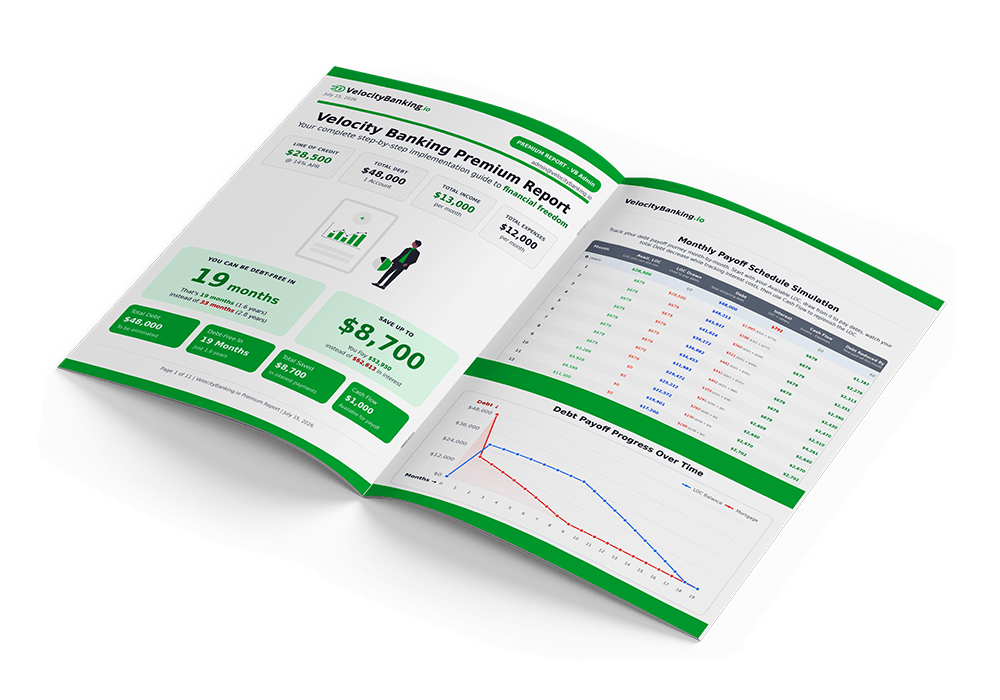

Use a line of credit (HELOC or PLOC) strategically, to eliminate debt and save thousands in interest payments. Our free velocity banking calculator simulates exactly how much you can save and creates a personalized plan to become completely debt-free using smart AI calculation.

See Your Personalized

Debt-Free Plan

Run the free calculator to get your exact payoff date, total interest saved, and a step-by-step velocity banking plan built from your own numbers.

Try Velocity Banking Calculator Free

Try Velocity Banking Calculator FreeVelocity banking is a debt elimination strategy that uses a line of credit—typically a HELOC (Home Equity Line of Credit), PLOC (Personal Line of Credit), or business line of credit—to accelerate paying off high-interest debt like mortgages, car loans, student loans, and credit cards.

The core principle behind velocity banking is simple: instead of making small monthly payments where most of your money goes toward interest, you use a lower-interest line of credit to make large "chunk" payments that attack the principal directly. By reducing the principal faster, you reduce the total interest you'll pay over the life of the loan.

How Does the Interest Savings Work?

Most traditional loans (mortgages, auto loans) use amortization, meaning your early payments are 70-80% interest and only 20-30% principal. With velocity banking, you bypass this by making large lump-sum payments that go 100% to principal reduction.

Additionally, lines of credit like HELOCs calculate interest on your average daily balance, not a statement balance. This means every dollar you deposit reduces the interest you owe that day. When you deposit your entire paycheck into your HELOC and then pay expenses from it throughout the month, your average daily balance stays lower than if you kept money in a separate checking account.

Who Can Benefit from Velocity Banking?

Velocity banking works best for people with positive monthly cash flow—meaning your income exceeds your expenses by at least $500-$1,000 per month. The strategy also requires access to a line of credit with a lower interest rate than your existing debts.

Common candidates include homeowners with equity (for a HELOC), individuals with good credit (for a PLOC), business owners (for a business LOC), and anyone committed to becoming debt-free faster while maintaining financial flexibility.

Velocity Banking vs. Traditional Debt Payoff

Traditional methods like the debt snowball or avalanche focus on paying minimum payments plus extra toward one debt at a time. While effective, these methods can take 15-30 years. Velocity banking can reduce that timeline to 5-10 years by leveraging the mathematical advantages of lower interest rates, daily interest calculation, and large principal reductions.

The key difference is velocity—hence the name. You're not just paying off debt; you're accelerating the process by using strategic financial tools.

Pay Off Your Mortgage or Any Other Debt Faster

Instead of making minimum payments where most of your money goes to interest, velocity banking helps you pay off debt faster by strategically using a line of credit (HELOC or PLOC) to eliminate mortgages, credit cards, and loans years ahead of schedule—while keeping your money accessible for emergencies.

Pay Off Mortgage Earlier

Make large "chunk" payments directly to your principal instead of small monthly payments where 70-80% goes to interest. Cut your 30-year mortgage down to 5-10 years.

Save $50,000 to $200,000+

The average homeowner pays more in interest than the original loan amount. By paying off your mortgage early, you keep that money in your pocket instead of the bank's.

Get Out of Debt Safely

Unlike aggressive debt payoff methods that drain your savings, velocity banking keeps your line of credit available for emergencies—so you can pay off debt fast without financial risk.

Velocity banking works for people who want to pay off their mortgage early or eliminate other debts faster than traditional methods allow. The strategy can be implemented with either a HELOC (Home Equity Line of Credit) or a PLOC (Personal Line of Credit), depending on your situation.

Requirements for Velocity Banking

- Positive monthly cash flow: Having at least $500-$1,000 remaining after all expenses is essential for the strategy to work effectively

- Access to a line of credit: This can be a HELOC (if you own a home with equity) or a PLOC (available to renters and homeowners alike with good credit)

- Credit score guidelines: Typically 680+ for HELOC approval, 700+ for personal lines of credit

- Consistent income: Regular paychecks help make the strategy predictable and easier to manage

HELOC vs. PLOC for Velocity Banking

Both types of credit lines can be used effectively. A HELOC typically offers lower interest rates (6-9%) and higher credit limits since it's secured by your home equity. A PLOC has slightly higher rates (10-15%) but doesn't require home ownership, making it accessible to renters who want to pay off debt faster.

Typical Debt Payoff Timelines

Results vary based on your cash flow and debt amounts, but here are examples of how velocity banking can help you get out of debt faster:

- $200,000 mortgage: Traditional = 30 years | With velocity banking = 7-12 years

- $300,000 mortgage: Traditional = 30 years | With velocity banking = 10-15 years

- $50,000 credit card debt: Traditional = 15+ years | With velocity banking = 3-5 years

Want to see your personalized timeline? Try our free velocity banking calculator to estimate how quickly you could pay off your mortgage or other debts.

How Does Velocity Banking Work?

A 4-step process to accelerate debt payoff and achieve financial freedom years faster than traditional payment methods.

Take a Chunk

Use your HELOC or PLOC to pay off a chunk of high-interest debt immediately.

Direct Income

Deposit your paycheck into the line of credit to reduce the balance you're paying interest on.

Use for Expenses

Pay monthly expenses from the HELOC/PLOC. Daily interest calculation saves you money long term.

Repeat Cycle

Each month your debt decreases faster. Repeat until completely debt-free using the velocity banking strategy.

Real-World Example

❌Traditional Method

$50,000 credit card debt at 18% APR

✅Velocity Banking

$50,000 HELOC at 7% APR

Our free velocity banking calculator helps you visualize exactly how much time and money you can save by implementing this debt elimination strategy. Here's what the calculator does and how to use it effectively.

What You'll Enter

The calculator asks for your current debts (mortgage, credit cards, auto loans, student loans), your monthly income and expenses (to calculate your cash flow), and your line of credit details (available limit and interest rate). This information allows the calculator to simulate both traditional payoff and velocity banking scenarios.

What the Calculator Shows You

After entering your information, you'll see a side-by-side comparison showing: how many years until you're debt-free with traditional payments vs. velocity banking, total interest paid in each scenario, the exact dollar amount you'll save, and a month-by-month breakdown of your debt payoff journey.

Understanding Your Results

The calculator uses your positive cash flow to determine optimal "chunk" sizes—the large payments you'll make from your line of credit to attack your debts. It also factors in the interest you'll pay on your line of credit while you recover from each chunk payment.

Results are based on mathematical calculations using standard amortization formulas and daily simple interest calculations. Your actual results may vary based on interest rate changes, income fluctuations, and how consistently you follow the strategy.

Ready to see your personalized debt-free timeline? Try the free calculator now and discover how much faster you could eliminate debt.

Why Does Velocity Banking Work?

The strategy combines proven mathematical advantages with powerful behavioral benefits to create a debt elimination system that actually works.

Mathematical Advantage

Behavioral Advantage

Lower Interest Rates

HELOCs charge 6-9% vs. 15-25% on credit cards

Daily Interest Calculation

Interest calculated on average daily balance, not statement balance

Attack Principal Directly

Large chunks reduce principal instead of mostly paying interest

Maintained Liquidity

Keep emergency fund access through your line of credit

Psychological Motivation

See large debt chunks disappear quickly

Financial Discipline

Cash flow tracking improves spending habits naturally

Is velocity banking safe?

Velocity banking is a legitimate financial strategy, not a get-rich-quick scheme. The safety depends on your personal financial discipline. If you have stable income, positive cash flow, and the commitment to follow the strategy consistently, velocity banking can be very effective. The main risks involve using your home as collateral (with a HELOC) and potential interest rate increases on variable-rate credit lines.

What credit score do I need?

For a HELOC, most lenders require a credit score of 680 or higher, though some may approve scores as low as 620. Personal lines of credit typically require 700+. The better your credit score, the lower your interest rate—which directly impacts how much you'll save with velocity banking.

How much money do I need to start?

You don't need a large savings account to start velocity banking. What you need is positive monthly cash flow—typically $500-$1,000 or more per month after all expenses. This cash flow is what drives the strategy forward. You'll also need access to a line of credit, which requires either home equity (for HELOC) or good credit (for PLOC).

Can I use velocity banking without a HELOC?

Yes! While HELOCs are the most common tool because of their lower interest rates and higher limits, you can also use a personal line of credit (PLOC), a business line of credit, or even a 0% APR credit card (for shorter-term debt attacks). The key is having a revolving credit line with a lower rate than your target debts.

Have more questions? Visit our complete FAQ page or read our blog for in-depth articles on velocity banking strategies.

Trusted by Thousands Working Toward Debt Freedom

Real People, Real Results

See how velocity banking has helped others achieve debt freedom faster than they ever thought possible.

"We paid off $47,000 in credit card debt in just 18 months. The calculator showed us exactly how to structure our chunks and we followed the plan. Game changer."

"I was skeptical at first, but the math doesn't lie. We're on track to pay off our mortgage 17 years early. The free calculator convinced us to try it."

"Between student loans and car payments, we had $83k in debt. Used velocity banking with a PLOC since we rent. Debt-free in 3 years instead of 12."

Results vary based on individual circumstances including debt amount, interest rates, and cash flow.

Ready to See Your Velocity Banking Plan?

Use our free calculator to see exactly how quickly you could become debt-free and how much you'll save. Get your personalized debt payoff timeline in seconds.